HMO and PPO are two of the most commonly used acronyms in the health insurance space. Used to describe health insurance plans, you’ve likely run into these terms while looking for health insurance, looking for an in-network doctor, or reading through your job’s employee benefits guide.

But, what do these acronyms mean? How are they different? Is an HMO or PPO better? The answers depend on several factors, which we’ll explain below.

What is an HMO?

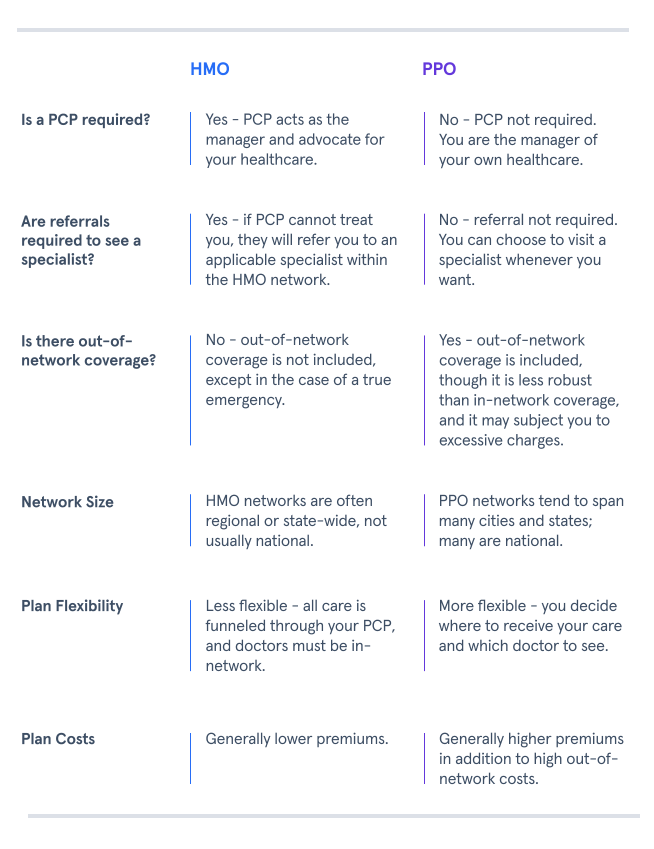

HMO stands for Health Maintenance Organization and can be more easily remembered by honing in on the word ‘maintenance.’

HMO health insurance plans help maintain your health by pairing you with a primary care physician (think of them as your maintenance manager) who will provide care and help you navigate the insurance plan’s network of doctors. In particular, your primary care physician (or PCP) will focus on preventive care and refer you to in-network specialists when more targeted diagnostic care is needed.

What are the Advantages of an HMO?

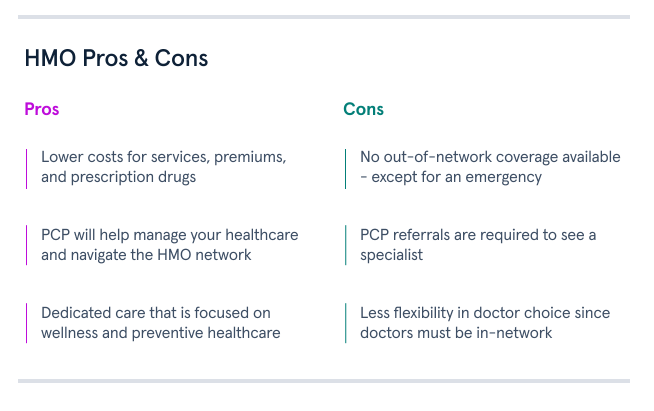

In addition to having a dedicated PCP to help navigate your care and doctor network, plan costs remain low since an HMO only covers in-network services. By forgoing out-of-network coverage, HMO members are subject to lower, in-network out-of-pocket expenses (deductibles, copays, and coinsurance) as well as a lower premium.

An HMO is especially applicable for budget-conscious people or those who only need basic medical care like annual checkups and preventive care. These individuals are comfortable forgoing the greater network flexibility of a PPO plan to enjoy dedicated, quality care at lower costs.

What is a PPO?

PPO stands for Preferred Provider Organization, and it is a health insurance plan that builds a broad network of medical providers to offer reduced out-of-pocket costs to plan members. Medical providers agree to join the plan’s network and honor the plan’s reduced rates in order to gain direct access to the plan’s member pool - thus becoming a ‘preferred provider’ of the medical plan.

What are the Advantages of a PPO?

Unlike HMOs that assign you to a dedicated in-network PCP and cover only in-network services, PPO health insurance plans offer greater flexibility by:

Eliminating the requirement of PCPs and PCP referrals.

Offering both in-network and out-of-network coverage.

While PPOs offer a preferred provider network, members are not restricted to that network and may venture outside if desired. These characteristics provide members with more choice and flexibility to navigate their own healthcare without the help of a PCP.

Greater flexibility also brings higher costs. PPO plans tend to charge higher premiums because they cost more to administer and manage. Moreover, members are subject to higher out-of-pocket costs when visiting providers outside the plan’s network, as those providers are not contracted to honor the plan’s reduced rates.

PPO plans are great options for those with more complex or specialized medical care needs that may require access to a broader, more flexible plan network. These individuals are comfortable paying a higher premium to gain access to greater network flexibility and choice.

HMO vs PPO: Which is Better?

Choosing between a PPO vs. an HMO health plan depends on several factors, including the state of your current health and healthcare needs, how you prefer to manage your healthcare, and your budget.

An HMO offers dedicated, quality care at lower costs led by an assigned PCP advocating for preventive care, wellness, and other referral services on your behalf.

A PPO offers greater network flexibility and doctor choice at higher costs to meet more complex or specialized care needs.

Ultimately, the choice can be boiled down to the lower cost of an HMO plan versus the greater flexibility of a PPO plan.